The financial sector of any economy is very different than any other sector. It supplies the key ingredients for all of the other sectors of the economy: Capital! Any problems in this sector rapidly disseminates to all of the other sectors of the economy. If credit or investments dry up because of issues with the financial institutions, it can bring down the entire economy. Two examples of that in the last 100 years are the Great Depression and the Great Recession. Those recessions were much more severe than any of the other recessions because of the fact that they started in the financial sector. US and western European economies have more developed and sophisticated financial sectors that operate efficiently and are well-regulated. This is one of the foundations of developed economies and absolutely necessary for long-term economic growth.

China’s financial sector is different than most developed economies. The Communist party and the central government in China have a very tight control of this sector and intervene in its functioning. This takes the form of ordering them to tighten or loosen credit and to whom they should extend credit to. This has allowed them to control the impact of the downturns in the economy better than most other countries. This, of course, comes with the downside that credit and investment may not always go to the best companies, but to the most connected and those that pledge full loyalty to the central government. Many economists have expected that this inefficient form of capital allocation would catch up with China sooner or later.

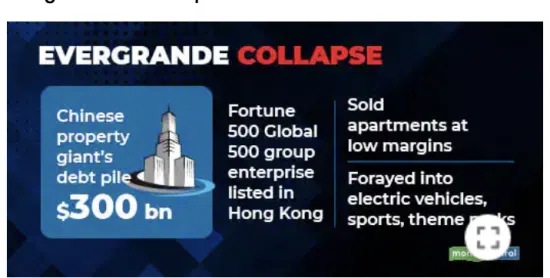

Since 2008, China’s credit-to-GDP ratio has rocketed from 140% to 290%. This could be the harbinger of trouble ahead. We have already seen this with Evergrande, a Chinese real estate company. Evergrande, a darling of the Chinese government and a symbol of their increasing economic might and international influence, collapsed last year. The company was able to continue to raise debt, even when its growth and performance would have made it hard for it to get access to so much credit. However, being connected to the central government has its perks. The result? At some point it could no longer could continue to service its debt because its operations were not as profitable as they needed to be to support that much debt. This is what happens when credit is extended not to the most efficient and high performing companies, but to those who stay close to government officials.

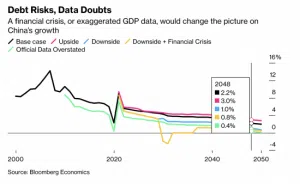

Bloomberg Economics estimates that a Lehman-style meltdown could push China into a deep recession followed by a lost decade of close to zero growth. Also, there is reason to believe that China’s stated growth numbers might be lower than reported (though not dramatically lower!) A study by economists at the Chinese University of Hong Kong and University of Chicago suggested that between 2010 and 2016, China’s “true” GDP growth was about 1.8 percentage points below what the official data suggested.

I have a few observations about all of this. For a long time, many people have predicted that all of these underlying issues in China’s financial sector will doom their growth prospects. China has been able to defy these dire predictions and has kept growing, many times by doing even more interventions by the central government. This is kicking the can down the road. At some point, you can no longer cover up for your earlier mistakes by ordering the banks to give even more credit to failing companies. Evergrande may be the first domino in a downside scenario that many have predicted. Most economists think there is a bunch more Evergrandes out there. An inefficient financial system will not be able to support China’s growth beyond a certain level. That’s because it is much harder to grow your GDP per capita beyond a level (~ $15,000) without certain key foundations, one of which is a sophisticated financial sector. Lastly, China’s Communist party is only getting more aggressive in interfering with the private sector in recent years. This means more mismanagement and misallocation of capital. Not a recipe for success but maybe they’ll keep proving us wrong again!

I go back to a point I have made many times: US needs to focus on improving its own economic growth through public sector investments and private sector reforms.